India's $300B AI Shock

What Is This and Why Should I Read It?

India’s $300 billion IT-BPO industry built much of urban India’s tax base, consumption engine, foreign-exchange cushion, and middle-class mobility story. As is already visible, AI is disrupting India's IT-BPO industry and hollowing out the wage pyramid underneath by reducing fresher hiring and replacing large delivery benches with much smaller teams. India needs to acknowledge that its most successful economic engine has become less labor-intensive and take urgent measures to establish industrial infrastructure for the AI era.

About The Author

Since 2023, Aman Kai Sidhant has invested in hardware, data and software companies that are beneficiaries of the AI supercycle at a US-India crossover fund. Previously, he was a Product Manager at Microsoft Azure.

Part 1: Why AI Comes for India’s Best Jobs First

Prologue: The Income Stream that Built Urban India

How IT-BPO Contributed to India’s Economy, and Why AI Puts that at Risk

I spent a lot of my formative years in Gurgaon and feel like I grew up with the city. For readers unfamiliar with Gurgaon, imagine spending your high school years in Silicon Valley in the 1990s or Shenzhen in the 2000s. Every few months a new shopping mall, apartment building or office complex rose up and one could see the city develop in real-time. Even though I couldn’t properly articulate why this was happening, the energy and excitement was palpable.

The development of Gurgaon and other “IT cities” like Bangalore, Hyderabad and Pune are results of the white-collar services boom in the Indian economy that started in the 1980s with firms like Infosys, TCS and Wipro entering the IT-BPO market. Starting from 0 in the 1980s, India’s IT-BPO sector crossed $300 billion in revenues this year.

The industry came into its own after 1991, when India opened its economy after decades of protectionism and created policies such as the Software Technology Parks scheme that incentivized global companies to outsource software, customer support, accounting, HR, and back-office work to India. Overseas companies bought white-collar services from Indian firms, and those firms paid millions of Indian workers salaries large enough to buy apartments, cars, school seats, restaurant meals, flights, insurance, and mutual funds.

In this essay, I want to explore the risk that India’s IT-BPO industry and workforce faces from AI. This is a double whammy to India’s economy because India’s Current Account is structurally vulnerable to IT-BPO export revenue, and IT-BPO workers are a small but disproportionately large domestic consumer base. Even if firms somehow continue winning contracts by pivoting to AI-enabled services, AI lets firms produce the same services with fewer workers, fewer freshers, smaller benches, and flatter wage ladders. The larger risk is that the IT-BPO industry’s revenue may substantially decline from current levels because the unit of work they sell has been commoditized by AI. Therefore, India must make it a sovereign priority to invest in industrial infrastructure that can power AI.

Coding is the first widespread commercial use case of AI and it’s just the beginning. Claude Code went from 0 to $1B in 7 months and then to $2.5B annualized revenue in less than 3 months. It took Cursor nearly 2 years to get to $1B annualized revenue and less than 3 months after that to get to $2B. OpenAI’s Codex has 5M+ weekly active users, up 6x since February 2026.

The same logic extends beyond coding. Customer support, finance and accounting, HR administration, document processing, compliance workflows, and general computer-use tasks are all exposed because they are structured, language-heavy, and historically labor-intensive. These characteristics enabled India’s growth story because of India’s labor force but AI now puts all of this at risk.

Markets have recognized this. Teleperformance, a 10.2B Euro revenue BPO that makes most of its money from tasks like customer service is among the most shorted stocks in Europe according to the FT.

A shock to IT-BPO wages and the industry more broadly won’t stay limited to just the technology sector. Since 1991, foreign companies have paid Indian IT-BPO firms, those firms paid millions of Indian workers, and those salaries built a large part of urban India’s tax base, consumption base, and upward-mobility story. India’s formal income tax base is narrow and its upper-urban consumption class is small, economically powerful and a non-trivial percentage of this class works in IT-BPO. India’s current accounts are financed in large parts by IT-BPO and other white collar services exports. India’s education system produces huge numbers of engineers for a labor market where the largest formal entry-level absorption is IT-BPO. This channel will weaken because of AI.

AI should be treated as a sovereign economic priority for India. As demonstrated by Anthropic’s Project Glasswing, it increasingly looks like access to the best AI models will be limited to a select few governments and companies with the capacity to pay for it or leverage of some kind. Just as resources like oil, electricity and an educated workforce were structurally important for the sovereign security of a nation in the 20th century, access to cutting-edge AI will be important in the 21st century. Access to frontier AI, compute, data centers, and the surrounding semiconductor and power supply chains will shape India’s bargaining power in the coming century.

Why Workers Get Hit Before Firms…

AI Compresses Company Headcount Before it Compresses Company Revenue

My hypothesis is that there will be large workforce cuts, hiring freezes for new college graduates and wage stagnation for remaining employees across IT services firms and BPOs over the next 2-3 years. Companies will still retain a small number of client-facing account managers and salespeople for bringing in new deals, as well as staff engineers/architects to steer agentic engineering tools and be accountable for the software engineering work that isn’t coding.

Source: IBM Corporate Training, 1979

When a Fortune 500 company hires TCS to migrate a legacy system to the cloud, most of the billable hours are spent on implementation work like writing API endpoints, configuring environments and running test scripts. Codex and Claude Code are already great at these tasks and they are getting better, which means that IT services firms may not need as many engineers as they did previously.

For high budget IT projects, there is a lot of interpersonal communication and project management involved that will still need humans. A VP of Supply Chain at Coca Cola would still want to talk to a human to get status updates. In the near term, the population at risk are the hundreds of thousands of junior to senior-level software engineers spending 40 to 60 hours a week doing implementation work when Codex or Claude Code can run for 100 hours a week for much cheaper. Maybe even more if there are staff level engineers rotating shifts to prompt the AI.

Q4 FY26 earnings from TCS, Infosys, and Wipro reflect the patterns I’m worried about around revenue and headcount decoupling at India’s three largest IT services firms. TCS shed roughly 23,500 net employees in FY26 while revenue declined 0.5% in USD.

Infosys lost 8,000 employees in Q4 alone, which was more than the entire year’s net addition of 5,000. Wipro quietly shifted its disclosure language from “230,000 employees” to “230,000 employees and business partners,” a phrasing change that makes their overall headcount harder to interpret. Combined Top-3 revenue is essentially flat in constant currency in a year when global enterprise AI spending is at record levels.

In FY24 and FY25, the consistent narrative across all three firms was that “AI is a tailwind” and a productivity enabler. On the Q4 FY26 earnings call, Infosys CEO Salil Parekh used “compression” five times. For example: “Compression is coming on some of the services and the growth is coming on other services. And the compression is typically in the areas where the AI foundation models and some of the tools are very efficient on that. So, you can see that in some of the tech services work, you can see that in some of the BPM work…”

The bull case is that AI is indeed a new revenue stream. TCS reported $2.3B in annualized AI revenue at Q4 FY26, roughly 7.7% of total. Infosys’ AI revenue is “higher than 5.5%” and growing, though management refused to update the Q4 number specifically. The narrative they want you to leave with is that legacy services are shrinking, AI services are growing, and the net is fine. Two problems with that. First, AI revenue almost certainly employs far fewer workers per dollar than the legacy services it’s displacing because these are tools-and-platform-heavy engagements, not body-shop staffing. Second, the AI base is still small relative to what it needs to offset. TCS’ non-AI revenue is roughly $27.7B, so even a modest 5% decline in that base is $1.4B of revenue that needs to be recovered. AI revenue would need to grow from $2.3B to $3.7B (a 60%+ jump) to keep the topline revenue for TCS flat, every year.

The fresher hiring decline is another leading indicator. TCS, the industry’s largest single employer, added a net 2,356 employees in Q4 FY26. This is the same firm that hired over 100,000 freshers in FY22. They also laid off 12,000 people and had 30,000+ net exits in 2025, the steepest decline in company history. Infosys, surprisingly, continues to hire. Wipro scaled back its college graduate (fresher) recruitment plans for FY26 and expected to hire ~8,000 graduates, compared to its earlier guidance of ~12,000. Overall, college graduate hiring for IT services in India has fallen from a peak of 600,000 in FY22 to about 120,000 in FY25. That’s an 80% (!) decline.

BPOs are also extremely vulnerable, and this is starting to show in official RBI data.

The Reserve Bank of India, India’s central bank, publishes revenue from Software and IT-Enabled Services Exports annually. Here is the report from the last 2 reported years (April 2023 to March 2025) -

Medical Transcription & Document Management reduced from $800M to $100M. That’s a 87.5% drop IN ONE YEAR. This coincided with the rise of several medical notetaking startups like Abridge and Ambience as well as big jumps in voice AI capabilities from the frontier labs.

Both HR Administration and Content Development are down 25% each, from $400M to $300M. Not as big a drop, but still concerning.

I may be overestimating the impact of AI on these cuts. Maybe the BPO revenue declined because of outsourcing to other countries like the Phillipines. Maybe customers have lower budgets for discretionary software development projects that IT Services companies build.

Having said that, it’s not implausible to imagine these cuts continuing in the wake of AI that is superhuman at digital tasks and coding. Early evidence is already visible in the US. Bloomberg recently reported that 17 occupations flagged by the Bureau of Labor Statistics as exposed to AI, covering roughly 9 million jobs, saw employment fall 1.6% between May 2024 and May 2025 for the second year in a row, even as overall employment in the US rose 0.8%. The sharpest losses were in BPO-adjacent roles that comprise large parts of India’s services-export machine: customer service representatives fell by 130,180 jobs, or 4.8%.

…And Firms Get Hit Eventually

India’s Body-Shop Model Loses Pricing Power because of AI

The immediate assumption to AI’s impact on IT-BPO is to assume that revenue will eventually decline because the core value proposition (cost arbitrage on coders) is now broken. IT Services firms are preparing for this new reality - TCS is starting to build AI data centers. From the press release and other online sources, it seems like TCS will build and operate purpose-built data centers where customers can place or run GPU-heavy AI infrastructure to run AI workloads. Essentially, instead of the output being code as it was traditionally, the core product for this business is real-world infrastructure.

This is a survival strategy for the firm, but not necessarily for the workforce. A data-center business can protect TCS revenue and shareholder value, but it does not need the same pyramid of junior engineers, project managers, testers, support workers, and freshers that traditional IT services did.

BPOs and GCCs might be more fragile than IT services, as we’ll see below.

IT Services

The strongest bull case for Indian IT services is that offshore human labor may remain more economical than frontier AI subscriptions, especially while model pricing is artificially subsidized by AI companies. But this assumes AI prices stay high and that clients keep buying labor-hours rather than outcomes.

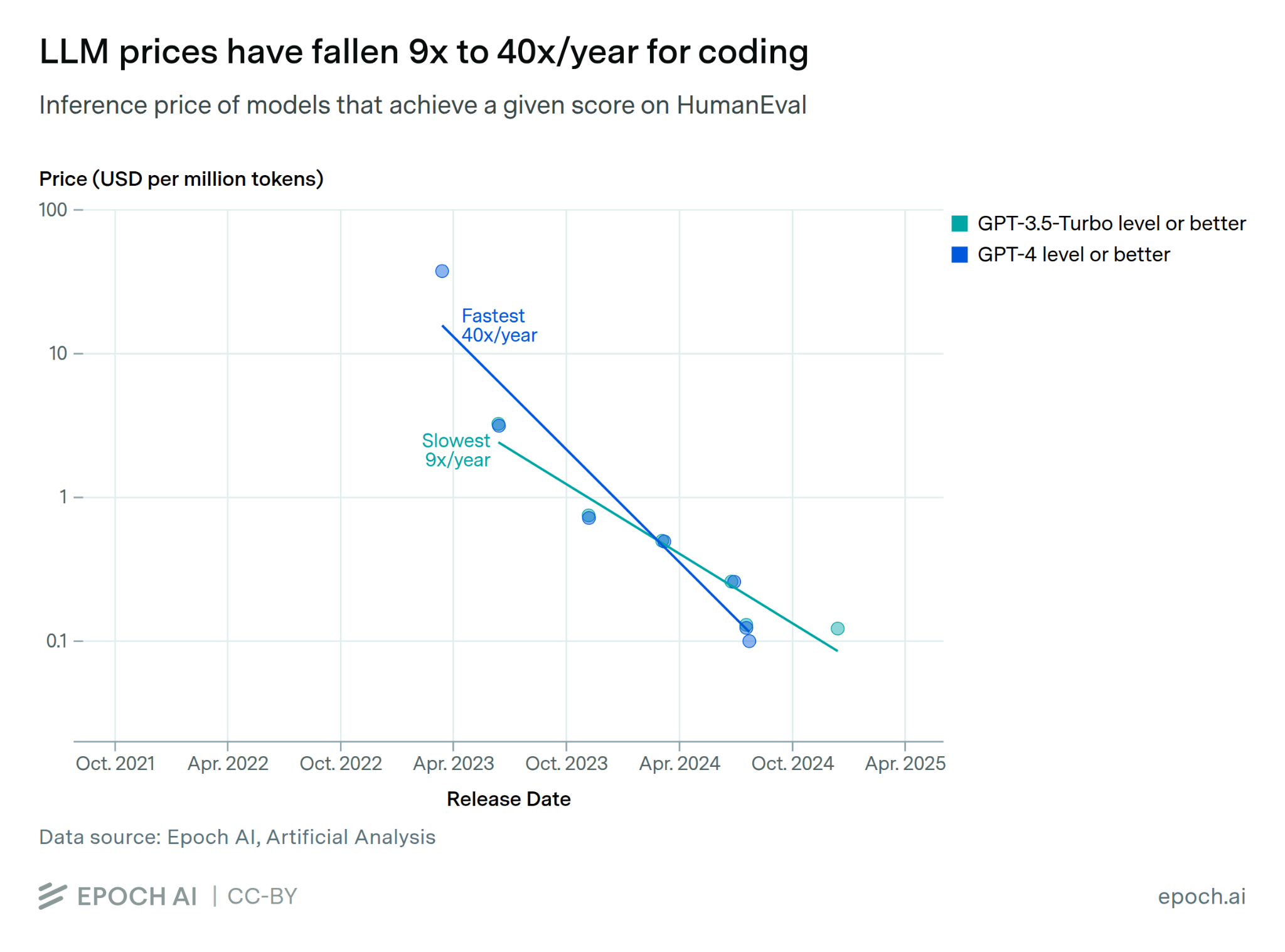

Let’s look at price levels for doing the same coding tasks -

https://epoch.ai/data-insights/llm-inference-price-trends

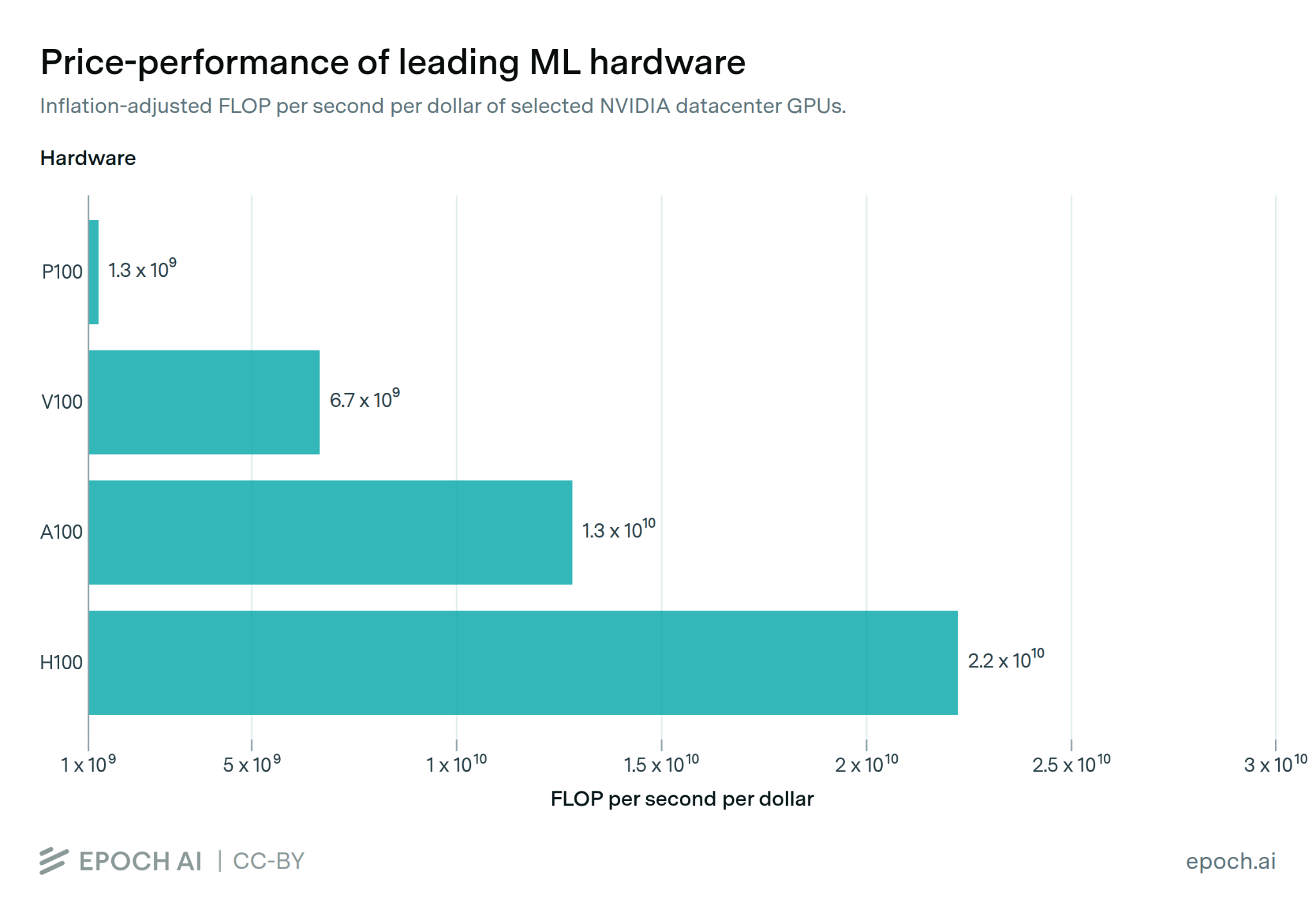

Let’s look at hardware -

https://epoch.ai/data-insights/price-performance-hardware

AI is getting cheaper through two reinforcing channels: first, the underlying hardware is improving steadily, with GPUs delivering roughly 30% more performance per dollar each year after adjusting for inflation and server costs. Second, the price of using LLMs at a fixed capability level is falling much faster, with the cheapest model/API price to hit given benchmark thresholds declining by 9x to 40x per year for coding. This makes it obvious to me that agentic engineering will reduce traditional IT Services revenue where the deliverable is code.

Another threat compounding this is that OpenAI and Anthropic have launched their own AI services firms in partnership with leading private equity and consulting firms. A big part of selling software to corporations was successfully creating a sales machine that can reach these corporations. This distribution was a big moat for large IT services firms vs. smaller firms because they had relationships with senior executives at most large corporations that have historically been buyers of services work. By partnering with Bain, Capgemini, McKinsey (in OpenAI’s case) and Accenture, Deloitte, PwC (in Anthropic’s case), OpenAI and Anthropic have circumvented the distribution challenge because these firms have the same relationships that an Infosys or Wipro has with corporations globally.

Let’s also understand why companies outsourced work to IT services firms in the first place, and how AI coding impacts all of them:

Converting Fixed Costs to Variable Costs

When companies hire full time employees (in the US), they are also responsible for their 401k, healthcare and other benefits, as well as severance and PR issues if the company goes through a downturn and needs to do a RIF. If instead of hiring 100 engineers you outsource that staff to Accenture or Infosys, downsizing and upsizing just involves talking to your account manager.

How AI affects this**:** Claude Code doesn’t sleep, can spin up subagents and output tokens 24/7 as long as the prompts keep coming. You might need an onsite solutions architect to collect project requirements and provide the big-picture context to Claude Code, but that’s it. Maybe 2 senior engineers to watch for tech debt from Claude Code’s output. The team of 30 is now a team of 3. This aligns with RBI’s data where only 9.3% of services output is on-site (same geography as the customer).

Build vs. Run

The best software engineers don’t want to maintain a Java app written 10 years ago. IT services firms were an easy way for enterprises to outsource boring “keep the lights on” work while their internal engineers worked on shiny new tech. This is why WITCH companies have a reputation for tedious, implementation-heavy work.

How AI affects this:

The tedious, implementation-heavy work that was the bread and butter of IT services firms is what agentic engineering tools excel at. There are still some rough edges around code review and AI sometimes making code tests pass in insidious ways like deleting test cases, but given the massive traction frontier labs are seeing from coding, these issues are likely front and center for them to solve next.

Skills at Scale

When a Fortune 500 company decides to migrate to SAP S/4HANA before the 2027 deadline, they need 150-300 SAP certified consultants for 18-24 months across dozens of modules. There is an entire ecosystem of consultants that exists because SAP is famously impossible to implement and work with while being extremely powerful. So powerful that Microsoft, despite having its own ERP product, uses SAP.

The same pattern applies to other software tools like ServiceNow and Salesforce as well as broader software practices like cloud migrations. No company maintains a bench of consultants or software engineers specifically for these workloads because these skills are only needed once.

How AI affects this: I’m not sure how much custom SAP logic was part of Claude Code and Codex’s training data, but Anthropic has already announced that Claude Code can modernize COBOL code cheaply despite the well-documented dearth of publicly available COBOL code. It is now clear that models have emergent capabilities that weren’t part of the explicit training goals simply as a consequence of general improvements.

If an AI agent can generate boilerplate SAP configuration, auto-generate test scripts, and handle documentation, a team of 150 becomes a team of 10. The IT services firm still wins the deal, but the deal is worth a lot less compared to what it used to be. Revenue per engagement compresses even if the number of engagements holds steady.

There are several startups attacking this problem too, which opens up IT services topline from multiple angles of attack. From a16z’s recent SAP piece:

Baked In Today, Replace Tomorrow

Investor Signaling

If outsourcing used to signal cost-efficiency and discipline to Wall Street previously, how long until analysts start asking CEOs about code-driven efficiencies in their internal engineering teams and outsourced IT contracts? The significant jump in coding abilities is fairly recent. I expect this to become more of an issue in the forthcoming quarters’ earnings calls. Block is frontrunning this with coordinated PR signaling that the recent 40% cuts were explicitly because of new agentic engineering capabilities.

How AI affects this: Obvious.

BPOs

BPOs will probably see the quickest disruption. We already saw the reduction in revenue for Medical Transcription & Document Management previously. BPO work is especially exposed because, unlike software engineering, it is harder to argue that AI simply makes existing workers more productive and allows firms to build more. Much of BPO is not “building” anything new. Customers generally want the same output at a lower cost, which is exactly the labor-arbitrage model that made Indian and Southeast Asian BPOs so successful in the first place. Even in India, API calls that can run 24x7 are cheaper and will produce better outcomes than hiring humans.

Let’s look at the RBI data again.

Several buckets within BPO Services actually grew. Business Consulting makes sense, since it is primarily advisory work and still requires significant human interaction. Finance also makes sense, since AI was likely not good enough by March 2025 to reliably handle critical tax, bookkeeping, compliance, and reconciliation workflows. Anecdotally, Codex and Claude Code have become extremely capable at Excel tasks for me, and frontier labs have made Finance tasks a priority for models. Since BPO contracts are often multi-year, contraction may not be immediately visible in RBI’s reports, but it is bound to happen.

Surprisingly (to me at least), Other BPO Services added $5B in export revenue. Based on the segmentation, I would assume this includes work like customer support, data entry and other back-office work. I think this bucket will see adverse impact starting this year.

Sierra, Bret Taylor’s company that started off selling AI agents for customer service, crossed $150 million in ARR in eight quarters and just raised at a $15 billion valuation. That kind of ARR multiple implies that Sierra is continuing to see tremendous growth and (speculation) is likely to expand to other use cases beyond customer service currently done by humans. Even if they don’t, the fact that customer service alone is a $400 billion market means that a lot of that revenue is going to go from companies where humans manage customer support tickets to companies like Sierra where AI does the work.

Several other AI-native customer service companies are also growing rapidly, and from due diligences I have done at work, AI already has a deflection rate of 50-60% for most Tier 1 support cases across voice and text.

GCCs

GCCs (Global Capability Centers) are a fancy way of saying offshore office. India is a hub for GCCs. From an Indian Government article in November 2025:

“India now hosts over 1,800 GCCs, representing 55% of the global total. These centres employ 1.9 million professionals and generate Rs. 5,72,873 crore (about $60 billion) in export revenue as of FY25. In total, the GCC sector supports 10.4 million jobs, with average salaries 25 to 30% higher than the national average.”

“By FY30, GCCs are expected to contribute nearly Rs. 8,86,800 crore (about $93 billion) in exports, underscoring India’s growing strength in innovation, compliance, and digital excellence.”

The GCC Sector in India supports 10.4 million jobs. That’s higher than the entire population of some European countries. GCCs are at risk for similar reasons we discussed above (Skills at Scale, Build vs. Run). And it’s starting already. Oracle laid off ~10,000 people in India recently, which is 20% of their entire Indian workforce. Sure, they’re spending a lot on capex, but they’re not going to RIF engineers if they didn’t have any alternatives ready to go.

Jevons Paradox and Radiology

Exploring the Counterargument

To steelman the other side ie IT Services companies will keep all their existing employees, and retrofit all of them with Codex 5.4 on extra high so they can build more.

This works if you’re a startup trying to build as much product as quickly as possible while keeping headcount low. It breaks down when you’re a publicly traded company responsible for maximizing shareholder value. If you’re an executive at Infosys, you have two options - either pay an average employee Rs. 15 lakhs (about $16,500) per year or pay Rs. 2.4 lakhs (about $2,700) for an annual Codex Pro subscription (likely cheaper on an enterprise-wide license). When your performance is judged on margins and earnings per share, the answer is obvious, and you will be outcompeted by firms that decide to rearchitect around AI.

When talking about the impact of AI on software engineer employment, many people cite Geoff Hinton’s argument around the risk to radiology that never panned out. Software engineering is fundamentally different. Fields like healthcare and law REQUIRE a human to be accountable for the final decision. Software engineering, particularly the cost-optimization kind that IT services firms sell, doesn’t require this degree of responsibility. BPO costs are even less safe because a company actively wants to reduce that spend as much as possible if it’s possible to do so with the same level of quality.

This excellent piece by David Oks explains that labor impacts due to technology happen not when the tasks get automated, but when the paradigm changes. That is a fancy way of saying that you need the entire workflow to change for technology to impact labor.

I posit that AI may have automated major parts of software engineering (writing code) but it hasn’t changed software engineering as a whole (yet). The reason this time may be different is that earlier waves of software mostly helped humans do the work faster. Excel did not replace the analyst, it made the analyst more productive. IDEs did not replace programmers, they made programmers more productive. AI agents are different because they increasingly perform the work itself: reading requirements, writing code, calling tools, generating tests, debugging errors, summarizing context, and iterating toward completion. Jevons paradox may still increase total demand for software, but the new demand does not necessarily flow back into human headcount if agents are the marginal workers satisfying it.

I believe coding agents are enough of a paradigm shift for the IT-BPO services workflow, where the entire pitch to customers is low-cost, scaled delivery rather than technical depth or architectural innovation. An increase in software demand can coexist with a collapse in the old offshore labor pyramid.

Anyone who has worked in a company will relate to this from Stratechery -

“It’s always been the case, even in large companies, that a relatively small number of people actually move the needle and drive the company forward in meaningful ways. That drive, however, has been filtered through a huge apparatus, filled with humans, who accelerate the effort in some vectors, and retard it in others. That apparatus makes broad impact possible, but it carries massive coordination costs.

Agents, however, will tilt much more heavily towards pure acceleration, making those drivers of value much more impactful. I’m sympathetic to the argument that the best companies will want to use AI to do more, not simply save money; the reality of large organizations, however, is that the positive impact of AI will not be in eliminating jobs, but rather replacing hard-to-manage-and-motivate human cogs in the organizational machine with agents that not only do what they are told but do so tirelessly and continuously until the job is done.”

What I think will happen (optimistically) - services firms will adopt AI as quickly as possible, with a select number of exceptional staff-level software engineers to steer the AI. These firms will win over the ones that stick to optimizing for billable hours and filling their bench with engineers.

The bear case is that companies bring the majority of this outsourced IT and BPO work in-house now that coding agents are more than good enough to do the median IT-BPO task.

To Recap

Both roads for an IT-BPO firm lead to the same place. In the bull case, the firm survives by re-architecting around AI and keeping a thin layer of staff-level engineers to steer it. In the bear case, the work vanishes entirely and is redirected to AI model companies. Neither road needs the pyramid of freshers, testers, and mid-level implementers the industry was built on. Even Jevons, right as it may be about total software demand, doesn’t route that demand back through human headcount.

Part 2 explores why a numerically tiny workforce punches far above its weight in India’s tax base, current account, and urban consumption.

Part 2: The Small Workforce Holding Up India’s Macro

Bloomberg recently released a newspost titled “Tata Boss Predicts AI Agents Will Replace Half Its Tech Jobs” based on comments made by Tata chairman N. Chandrasekaran at TCS’s shareholders meeting. While the headline is an exaggerated interpretation of what was actually said, it’s sobering to consider the implications of widespread labor displacement at India’s largest private employer. Below is a scenario that I think will play out in IT-BPO:

-

FY26/CY25 - Divergence. Hiring freezes and the first net headcount cuts (TCS alone shed 23,460 roles) while revenue keeps climbing. The labor shock is real but still invisible in the macro data.

-

FY27/CY26 - Acceleration. We are here Cuts spread beyond TCS, the fresher pipeline collapses (TCS cut graduate offers 43%), and revenue-per-deal begins to compress.

-

FY28/CY27 - Run-rate. Topline revenue decline turns visible, services-export growth stalls, and the current-account and tax channels start to transmit the shock.

-

FY29-30 - Compounding. Urban consumption softens, the rupee feels it, and unlike every past crisis, there is no reopening. The gap recurs every year.

The rest of Part 2 builds this scenario up from its constituent parts - the tax base, the current account, urban consumption, and the future tax base - before “Putting Everything Together” reassembles them and puts numbers on the drag.

A Small Labor Pool Props Up Indian Taxes, Dollar Reserves and Consumption

India’s IT-BPO workforce is roughly 5.8 million people. Compared to India’s labor force of 617.6 million, this population is <1%.

This workforce is also one of the most economically productive populations in the country. My bottoms-up analysis of TCS, Infosys, and Wipro’s FY25 employee benefit costs (a good proxy for employee compensation) from SEC 6-K filings gives a weighted-average compensation of Rs. 24.5 lakh (about $27,000) per employee. Taking into account average BPO salaries, the realistic weighted average for IT-BPO overall sits around Rs. 14.7 lakh (about $16,000) take-home, which is roughly 7.6 times India’s per capita Net Income of Rs. 1.93 lakh (about $2,000)

These 6 million workers occupy a critical junction across several economic systems, and contraction in any one channel can have disproportionate macro effects. IT-BPO workers are a small share of India’s labor force, but they sit at an unusually important junction: they earn high formal-sector wages, pay income tax, support upper-urban discretionary consumption, and generate foreign exchange through services exports.

-

Tax base: India had 75.46 million income tax filers but only 28.16 million paid positive tax in AY 2023-24. The IT-BPO occupational cluster of six million workers earning Rs. 14.7 lakh (about $16,000) average is overwhelmingly inside the positive-tax-paying 28 million people

-

Current Accounts: IT-BPO generates the bulk of the $204.7B in software services exports, which is India’s single largest source of net foreign exchange. On the other hand, India had a goods deficit of ~$280B in FY25. If IT-BPO export revenue growth slows from current trajectory, the rupee will depreciate, which feeds into oil and other import costs disproportionately borne by the entire population.

-

Urban Consumption: Blume Ventures’ frequently cited Indus Valley Reports frame India as three economies: India1 (~140M people, 10% of population, $15K average income, drives two-thirds of all discretionary spending), India2 (~300M people, drives the remaining third), and India3 (~1B people, largely outside the consumer economy). At Rs. 14.7 lakh (about $16,000) average compensation, IT-BPO workers sit squarely inside India1.

Tax Base

For the analysis here, I will look at data from 2024 since that is the latest available year with all the metrics I’ll need.

India’s individual income tax base is extremely concentrated. In 2024, India had 580 million employed workers and only 83 million people filed income tax returns. Of those, only 28 million actually paid income tax.

The IT-BPO workforce of 5.8 million (NASSCOM Strategic Review 2026) is overrepresented inside this 28 million population. My bottom-up estimates put IT-BPO at 17-20% of all salary TDS. For non-Indian readers, TDS is India’s version of deducting income tax from a worker’s paycheck.

This means IT-BPO, with less than 1% of India’s total employed workforce, contributes roughly 20% of India’s salary-withheld income tax!

When 23,460 TCS roles disappeared in FY26 and 12,000 Oracle India roles are eliminated, these workers likely go into a much lower taxation cohort if they become freelancers under Section 44ADA of the Indian Income Tax regime. A BPO worker would likely fall into informal services given their relatively lower skilled experience, and their income tax contribution goes to 0.

A structural reason for this asymmetry is India’s tax exemption for agricultural workers. Roughly 282 million agricultural workers (44.8% of CY 2024 employment per the PLFS Annual Report, MoSPI) are excluded from income tax collections, and often fall below taxable thresholds anyway.

The Future Tax Base

A second-order effect that operates with a 5-7 year lag is that the fresher hiring pipeline that turns engineering graduates into future high earners is contracting sharply. TCS, which is the largest private-sector employer of engineering graduates in India, cut its FY27 new college graduate (“Fresher”) target by 43% from to 25,000 from 44,000 in FY26. The fresher cohort itself contributes very little to current income tax (entry-level total compensation of Rs. 3.5-6L (about $3,000 - $7,000) are taxed at low rates) so most pay zero income tax in their first three years (their tax contribution is mostly through consumption-based taxes). The damage is to the future tax base. A fresher hired into TCS in 2018 typically reached Rs. 15-25L total compensation by 2025, entering the top-decile tax-paying tier. If fresher hiring reduces today, that impacts India’s future high tax-paying base.

GCCs cannot make up the gap, because GCC fresher hiring draws from a much narrower top-tier-college funnel and absorbs perhaps 20-30K freshers a year industry-wide versus the ~150K tier-2/tier-3 absorption that Indian IT services historically provided. India produces roughly 1.5 million engineering graduates per year, and if formal-sector employment narrows by half, the cohort feeding the Rs. 20L+ (about $22,000+) tax tier in 2030-2032 shrinks correspondingly. Besides, Indian GCCs are going through workforce displacement themselves, as seen with Oracle.

India’s income tax collection was constructed on an assumption of continuous formalization that would pull more workers from informal agriculture into formal services every year. IT-BPM was the engine of that pull for two decades, growing from ~1.3M workers in 2005 to 5.80M in 2024 while individual tax filings rose from ~25M to ~82M roughly in tandem.

If workforce displacement happens due to AI, India (and to be fair, most other countries) will look increasingly like a jobless growth economy where headline GDP may look fine but the consuming class shrinks.

Current Accounts

The IT-BPO sector is disproportionately relevant to India’s economic stability because it is one of the country’s most important sources of foreign-currency earnings. This is important because India imports far more physical goods like oil, electronics, machinery and gold than it exports, which means dollars are constantly flowing out of India to pay for the goods it buys from the rest of the world. IT-BPO helps replenish those dollars by selling services to global clients.

The current account is India’s foreign-exchange scoreboard. Every day, dollars leave India to pay for oil, electronics, machinery, gold and other imports. Dollars come back through goods exports, software and business-services exports, remittances, tourism and other cross-border income. The current account measures whether those recurring flows are broadly balanced. A small deficit is manageable, but a large or sudden deficit results in a weaker rupee, higher import costs, tighter policy, and government appeals to save fuel or buy less gold.

In FY2024-25, India’s merchandise exports were US$441.8 billion, while goods imports were US$729.0 billion, creating a US$287.2 billion goods-trade deficit.

India’s services economy moved in the opposite direction: services exports were US$387.5 billion, against services imports of US$198.7 billion, creating a US$188.8 billion services surplus. IT-BPO is central to that surplus. RBI’s FY2024-25 software and IT-enabled services export survey estimates India’s software services exports at US$204.7 billion. That services surplus is one of the main reasons India’s overall current-account deficit was only US$23.3 billion, or 0.6% of GDP, in FY2024-25.

April 2026 showed how quickly the current account deficit can impact day-to-day life for Indian citizens. Amid the Middle East energy shock, India’s monthly merchandise trade deficit widened to $28.38 billion, up from $20.6 billion in March. Imports rose to $71.94 billion, with oil imports alone rising to $18.62 billion from $12.18 billion in March, while gold imports stood at $5.63 billion. The rupee fell below 96 per dollar after the data. India’s external account is structurally exposed to oil and gold, and software/services exports are one of the few large recurring dollar inflows that offset that exposure.

In response, the Government had to raise retail fuel prices for the first time in four years, tighten gold imports to reduce foreign-exchange outflows, and PM Modi urged citizens to cut fuel use and reduce gold purchases. AP separately reported a ₹3/litre fuel-price increase, gold and silver import duties raised to 15%, and a 90-day fuel-saving campaign with work-from-home days for some government employees in Delhi. If the services-export cushion from IT-BPO weakens, India has less room to absorb oil, gold, electronics, and geopolitical shocks without currency pressure.

IT-BPO is the single biggest source of foreign money the country earns. Without it, India would be buying roughly twice as much from the world as it sells back. A gap that big is only possible as long as dollar reserves are available and overseas capital is willing to give India loans and investment. Such dependence on overseas investment isn’t sustainable, as is evident from the outflow of foreign investment capital from India in the last year.

We’ve already seen an 83% decline in Medical Transcription BPO revenue. What happens if there’s a 50% cut to IT/BPM exports? This means a first-round loss of about US$102.4 billion. Hold everything else constant and India’s services surplus falls from US$188.8 billion to about US$86.5 billion. The current account deficit widens from US$23.3 billion to roughly US$125.6 billion, which is about 3.2% of GDP.

What happens then? India has seen this before in 1991 and 2013. In FY1990-91, a current account deficit of 3.1% of GDP became unsustainable and led to an external payments crisis that saw India literally flying gold to the Bank of England to collateralize its debts and eventually led to India’s liberalization.

The deficit reached a peak of 4.8% of GDP in FY2012-13 when US Federal Reserve Chair Ben Bernanke told Congress the Fed might start slowing its bond purchases. India had done nothing wrong that quarter. IT services were healthy. Exports were growing. But US interest rates suddenly looked more attractive, foreign investors reassessed the risk of holding Indian assets, and the rupee fell 7.5% against the dollar between May 22 and July 15 2013. The RBI burned through reserves, launched emergency dollar deposit schemes targeted at NRIs, and tightened monetary policy.

If AI breaks IT services, India faces two problems at once. The first is lower export earnings which widens the current account deficit. The second is that IT services have been India’s growth story for foreign investors. Three decades of India’s pitch to global capital has been “India is the world’s services back-office and its technology division”. As AI improves and breaks the pitch, foreign capital will rotate to countries that have more data center and semiconductor capacity.

Foreign capital is already leaving

FY2024-25 wasn’t a great year for Foreign Institutional Investor (FII) inflows into India’s stock markets even without any IT-BPM declines. Gross FDI inflows were strong at about US$81.0 billion in FY2024-25, but net FDI inflow fell to just US$1.0 billion, down from US$10.2 billion in FY2023-24 and far below the US$43.4 billion India recorded in FY2020-21. RBI’s balance-of-payments data show FPI net inflow of only US$3.6 billion in FY2024-25, down from US$44.1 billion a year earlier. That weakening is visible in market ownership as well. By September 2025, foreign portfolio investors owned only 16.9% of NSE-listed companies, which NSE data described as the lowest in more than 15 years.

Why is this happening? An HSBC note described India as a “funding market” for Asia’s AI boom, with capital getting out of India and into South Korea and Taiwan. Nearly $28 billion had been withdrawn from Indian equities between September 2024 and November 2025, leaving India the second-largest underweight in global emerging-market portfolios. The underlying point is that foreign capital has already started rewarding markets with obvious semiconductor and AI winners more aggressively than India.

Urban Consumption

It is helpful to think of India not as 1 national consumption market but as 3 different markets. Ostensibly the market seems huge with 1.4 billion people, but India’s monetizable market is much smaller.

Blume Ventures, an Indian VC firm, releases fantastic Indus Valley Reports about the Indian economy and startup ecosystem. Most readers working in Indian startups are likely familiar with them. From their March 2025 report:

The top ~10% of India, named “India1”, has roughly 140 million people with per-capita income of $15K and drives 2/3rd of all discretionary spending.

The next 21%, the rising “India2”, drive the remaining 1/3rd of discretionary spending with per-capita income of $3K.

This reflects in per-capita over-indexing. The consuming “India1” class spends: 3-5x the national per-capita rate on basic categories (food, fuel, clothing), 7-9x on consumer services, conveyance, education, 10-13x on jewellery, out-of-home food, institutional medical, durable goods. A shock to incomes inside that group will have a disproportionate impact on GDP. We know from the beginning of this section that India’s IT-BPO workforce is roughly 5.8 million, with an average take-home salary of Rs. 14 lakhs (~$15,000). Taking into account double-income households and supporting immediate family like children and parents, let’s assume these 5.8 million workers are supporting 15 to 20 million people. Taking the lower bound of 15 million, that is 10% of “India1”, the group driving 2/3rd of Indian discretionary consumption, directly dependent on IT-BPO salaries.

The first-order impact on IT-BPO workforce displacement will likely show up in IT cities like Bangalore, Hyderabad, Gurgaon, Pune and Chennai. Bangalore and Hyderabad alone have anywhere from 2 million to 2.5 million of India’s 5.8 million IT-BPO workers. These cities also sit at the center of India’s consumer-internet monetisation map, whether the product is food delivery, fintech, travel, quick commerce, or premium retail.

To be clear, these cities also have several other high-value industries like pharma, manufacturing and financial services (which may have its own reckoning now that models are good at Excel), but IT-BPO is the most likely marginal employer of the cohort with the highest urban discretionary propensity - fresh graduates, dual-income couples in their late 20s and mid-career professionals in the Rs. 15-80L (about $16,000 to $90,000) bracket.

What happens when the marginal salaried spender in India’s five most important tech cities sees slower income growth? When that pipeline slows, this cohort’s incremental spending, which has been funding the growth in consumer company P&Ls (both startups and old-school enterprises), will also decline.

Many Indian consumer internet business models also depend on “India1” contribution margins to finance “India2” expansion. That has been the operating logic of much of India’s consumer startup ecosystem for the last decade: acquire and monetise dense upper-urban users first, then use that cash flow, network density, and logistics base to push outward.

A slowdown in upper-urban salaried demand could impact businesses whose long-term growth story is to expand beyond India’s big cities. If the high-frequency, high-margin urban user base weakens, the company has less room to spend on expansion, subsidies, assortment, merchant acquisition, dark-store density, or customer support in lower-yield markets. Thus, “India2” also becomes harder and slower to monetise.

Putting Everything Together

At the start of Part 2, Chandrasekaran’s “half a million AI agents” gave us a five-year arc. We’ve now walked each channel it travels through - the tax base, the current account, urban consumption, and the future tax base. Here is that same arc with the macro numbers attached.

A 1 to 5% GDP impact may ostensibly look small, but if it recurs annually until the Indian government takes measures to fix things, it will become a growth problem for India’s GDP by hitting sectors of the economy that produce formal wages, services exports, tax revenue and urban consumption.

The US dot-com recession is remembered as a major financial-market event, yet the GDP impact was shallow: the recession lasted from March to November 2001, and real GDP barely declined. The 2008 Global Financial Crisis was much more severe: US real GDP fell roughly 4% from peak to trough, and the recession lasted 18 months. India’s Covid shock was larger still: real GDP contracted 5.8% in FY2020-21 before rebounding the next year. Even a 1 to 2% annual drag on GDP is much larger than the GDP imprint of many famous economic downturns. A 4 to 5% drag belongs in the same numerical range as crises that governments and markets treat as historic events.

However, the historical comparisons actually understate the AI risk in an important way. Most crises have a beginning, a trough and a recovery phase. Covid had reopening. The Global Financial Crisis had bank rescues, monetary easing and fiscal stimulus. Even when the recovery was painful, there was a policy and business-cycle mechanism pushing the economy back toward normal.

AI displacement is different because of recurrence. This is not like a factory shutting down for a quarter and then reopening. If AI permanently automates a support process, a testing team, or a back-office workflow, the wages attached to that work do not automatically return next year. The spending supported by those wages does not automatically return either. India has to create a new source of income to replace the old one. Until that happens, the gap keeps appearing every year.

The impact on incremental GDP growth is also illustrative. Suppose India’s GDP is at $100 today. If nominal GDP is expected to grow 8.6% next year like it did in FY 2025-26, the economy should get to 108.6 next year. A 2% GDP drag means the economy reaches about 106.4 instead. India still grows, but almost 25% of the expected annual increase has disappeared.

Investors underwrite India on the belief that nominal GDP will keep expanding fast enough to support corporate revenue growth, tax growth, credit growth, infrastructure spending, urban consumption and rising market size. If AI displacement removes 25 to 50% of expected annual nominal growth, the effects travel beyond the workers directly displaced. Corporate revenue expectations weaken. Tax buoyancy weakens. Credit quality weakens. Urban consumption slows. The denominator that makes public debt, infrastructure spending and private capex look manageable grows more slowly. India can still grow, but the premium attached to India’s growth story becomes harder to justify.